Share Market News, IPO News: Exchange of stocks SME listing requirements are now more stringent thanks to NSE. According to the exchange, SMEs who wish to list their securities on NSE EMERGE, its SME platform, would now need to meet a few more standards.

NSE Strengthens SME Listing Criteria with New

IPO News, Share Market News: NSE Strengthens SME Listing Criteria with New

On Thursday, the National Stock Exchange (NSE) of India implemented more stringent guidelines for small and medium-sized business (SMEs) listing.

The bourse announced in a circular that in order for SMEs to list their securities on NSE EMERGE, its SME platform, they will now need to meet a few more standards.

Free cash flow to equity (FCFE) for the company or entity must have been positive for at least two of the three fiscal years prior to the application NSE said.

The current requirements will be supplemented by this one.

According to NSE, the extra requirement will be applicable to all draft red herring prospectuses (DRHPs) submitted on or after September 1, 2024.

Every other criterion stays the same. This will remain in effect until further directives,” the NSE stated.

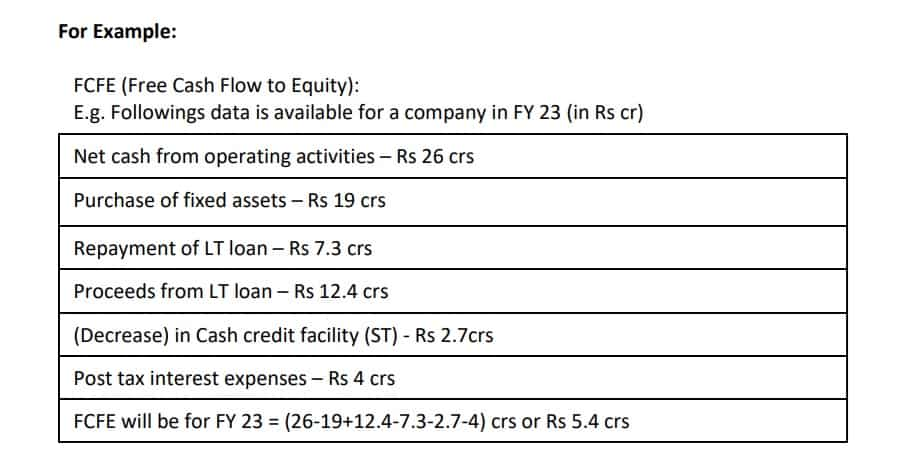

The NSE provided the following methodology details for calculating free cash flow to equity (FCFE): , NSE Strengthens SME Listing Criteria with New

FCFE is equal to cash flow from operations plus net borrowings less interest times one-time (one-to-three).

- The calculation of operating cash flow will be as follows:

Net Cash Flow from Operating Activities is the sum of Cash Generated from Operating Activities and any applicable income taxes.

- Acquisition of Fixed Assets will be calculated as:

Acquisition of Plant and Equipment (PPE) and Capital Works in

Progress (CWIP))-Money from the sale of PPE, any CWIP, and any capital advances

- Net Borrowings are going to be calculated as:

Repayments of Long-Term Borrowings + Proceeds from Short-Term Borrowings – Short-Term Borrowings Repayments = Proceeds from Long-Term Borrowings

- Interest multiplied by (1-T) will be found as:

Interest Charged on Total Borrowings (including Short- and Long-Term) x (1 – T#)

- T is the company’s effective tax rate:

Calculating the Effective Tax Rate as [1-(PAT/PBT)]

“All the figures and numbers will be taken from audited balance sheets (filed with offer documents) only,” it stated.

An example was also provided in the exchange to clarify the methodology:

NSE EMERGE: What is it?

Emerging companies can raise equity financing from a variety of investors, including institutional investors and high net worth individuals, using the NSE’s SME platform, EMERGE (HNIs). (NSE Strengthens SME Listing Criteria with New)

Account opning link:

- Groww Account- https://app.groww.in/v3cO/kyrp1zph

- Kotak neo Account https://kotaksecurities.ref-r.com/c/i/32531/109103906

Table of Contents

My name is Nitesh kumar and i am a Engineer but i have passionate in blogging, so these website updates day to day publish in stocks news and ipo’s and business related news update.

“Stock24News.com is your premier source for real-time financial updates and market insights. Stay informed with our expert analysis and comprehensive coverage of global stock trends.”

Thanks for your visiting in stock24news.com